How to Create a Debt Snowball Strategy to Pay Off Debt Faster

When it comes to getting out of debt, it can feel like an overwhelming and insurmountable task. With multiple credit cards, loans, or bills piling up, it’s hard to know where to begin. One effective method that has helped many people regain control of their finances is the debt snowball strategy. This approach not only simplifies debt repayment but can also keep you motivated as you see progress along the way. If you’re looking for a way to pay off debt faster and gain financial freedom, the debt snowball method could be the solution you need.

What is the Debt Snowball Strategy?

The debt snowball strategy is a method of paying off debt where you focus on paying off your smallest debt first while making minimum payments on all other debts. Once the smallest debt is paid off, you move on to the next smallest debt, and so on. As you pay off each debt, the amount of money you can apply to the next one increases—like a snowball rolling downhill, gaining momentum.

Why the Debt Snowball Strategy Works

-

Psychological Boost: Paying off a debt, no matter how small, gives you a sense of accomplishment. This can boost your confidence and provide the motivation needed to keep going. The quick wins can help maintain momentum and turn the task of debt repayment from an overwhelming burden into an achievable goal.

-

Simplified Focus: By concentrating on one debt at a time, the strategy eliminates confusion and makes the process less daunting. You don't have to worry about juggling multiple debts with varying interest rates or repayment schedules.

-

Increasing Payments: As you pay off each debt, you free up more money that can be applied to the next debt in line. This "snowball" effect makes your repayments grow exponentially, helping you pay off debt faster.

How to Create a Debt Snowball Strategy

Here are the steps you can follow to create and implement a debt snowball plan:

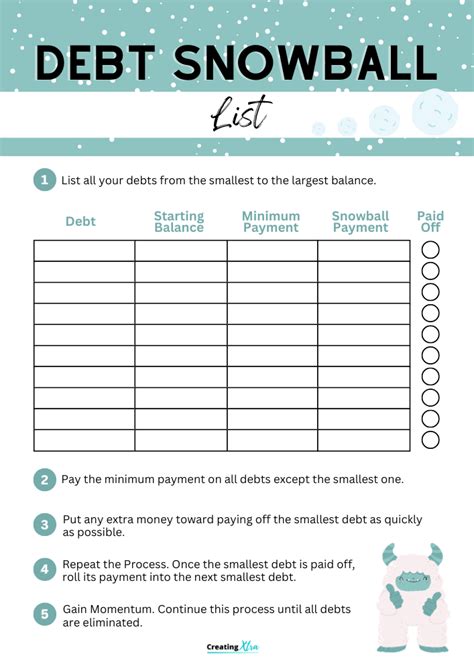

List All Your Debts

Start by making a list of all your debts, including credit cards, loans, medical bills, etc. Include the following details for each debt:

- Creditor/Loan Provider: Who you owe money to.

- Total Balance: How much you still owe.

- Minimum Payment: The minimum payment required each month.

- Interest Rate: The interest rate charged on the debt.

Order Your Debts from Smallest to Largest

Once you have your list, arrange your debts from the smallest balance to the largest. The idea behind the debt snowball strategy is to focus on paying off the smallest debt first. The size of the debt, rather than the interest rate, is the key factor here.

Make Minimum Payments on All Debts Except the Smallest One

For each debt except the smallest, make only the minimum required payment. This ensures you're still making progress on all your debts while focusing most of your financial energy on the smallest debt.

Throw Extra Money at Your Smallest Debt

Now, put any extra money you can find into paying off your smallest debt. This could mean cutting back on discretionary spending, finding additional income, or reallocating funds from other areas of your budget. The goal is to throw as much money as you can at this smallest debt to pay it off as quickly as possible.

Move on to the Next Debt

Once the smallest debt is paid off, take the amount you were paying toward it and add it to the minimum payment for the next smallest debt. This creates a snowball effect, where your payments grow larger and larger as you continue to pay off each debt.

Repeat the Process

Continue the process of paying off your debts in order of size, while redirecting the funds you were paying on each debt to the next one. As you progress, you’ll find that your payments increase, and you’ll be able to pay off your debts faster than you initially thought possible.

Celebrate Your Progress

As you pay off each debt, take a moment to celebrate. Each time you pay off a debt, you’re one step closer to becoming debt-free. These milestones will help keep you motivated as you continue on your debt-free journey.

Tips to Maximize the Debt Snowball Strategy

-

Track Your Progress: Regularly track your progress to see how much you’ve paid off and how much closer you are to financial freedom. This will help keep you motivated and focused on your goal.

-

Avoid New Debt: As you focus on paying off your current debts, avoid taking on any new debt. Using credit cards or taking out loans can derail your debt snowball efforts and make it harder to achieve your goal.

-

Use Windfalls Wisely: If you receive any unexpected income—such as a tax refund, bonus, or gift—use a portion or all of it to pay off your debts. This can give your snowball a major boost.

-

Refinance if Possible: If you’re struggling with high-interest debt, consider refinancing options or consolidating your debt to lower the interest rates. While the debt snowball focuses on the size of the debt, refinancing could help speed up the process by reducing the amount you pay in interest.

Debt Snowball vs. Debt Avalanche: Which Is Better?

You might come across another popular debt repayment strategy called the debt avalanche. The main difference between the two is that the debt avalanche method prioritizes paying off the debt with the highest interest rate first, rather than the smallest balance.

While the debt avalanche can save you money on interest in the long run, the debt snowball strategy tends to offer quicker psychological wins by paying off smaller debts faster. If you need motivation and a sense of accomplishment to stay committed, the debt snowball may be a better choice.